Article 6 Income from Immovable property – Transaction Envisaged

KEY QUESTIONS

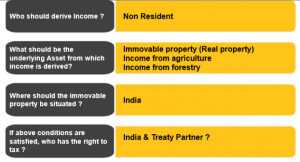

- Immovable Property Covered ?

- Right of India to Tax

- Right of Treaty Partner to Tax

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

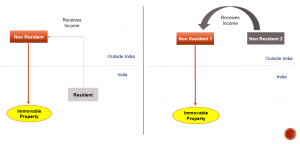

ARTICLE 6(1) – INDIA USA – RIGHT OF INDIA AND US (FOREIGN STATE) TO TAX IFIP

Income derived by a resident of a Contracting State (NR)

from immovable property (real property),

including income from agriculture or forestry

situated in the other Contracting State (India)

may be taxed (both States have right to tax)

in that other State (India)

ARTICLE 6(3) – NATURE OF INCOME FROM IMMOVABLE PROPERTY COVERED UNDER ARTICLE 6

The provisions of paragraph 1

shall also apply to

income derived from the

direct use,

letting, or

use in any other form

of immovable property

KEY ISSUES IN ARTICLE 6(1)

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

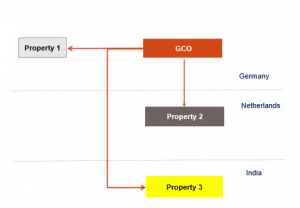

CASE 1 – WOULD INDIA GERMANY TREATY APPLY TO PROPERTY 1 & 3 ?

WHAT IS THE MEANING OF “INCOME” ?

- Definition of Section 2(24) of the IT Act 1961

- “Use” of immovable property could be in any form

- Transfer of immovable property and gains thereon covered by Article 13

“MAY BE TAXED” – PROTOCOL TO THE INDIA MALAYSIA TAX TREATY

It is understood that

the term “may be taxed in the other State”

wherever appearing in the Agreement

should not be construed as preventing

the country of residence

from taxing the income.

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

ARTICLE 6(2) – MEANING OF IMMOVABLE PROPERTY

The term “immovable property”

shall have the meaning

which it has under the law of the Contracting State

in which the property in question is situated.

ARTICLE 6(2) – MEANING OF IMMOVABLE PROPERTY

The term shall in any case include property accessory to immovable property, livestock and equipment used in agriculture and forestry, rights to which the provisions of general law respecting landed property apply, usufruct of immovable property and rights to variable or fixed payments as consideration for the working of, or the right to work, mineral deposits, sources and other natural resources

ships, boats and aircraft shall not be regarded as immovable property

ARTICLE 6(4) – PROPERTY USED FOR PROVDING IPS

The provisions of paragraphs 1 and 3 shall also apply

to the

income from immovable property of an enterprise and

to income from immovable property used for the performance of

independent personal services.

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

COMPUTATION OF INCOME IN SOURCE STATE

- Article 6 does not provide methodology of computing income in Source State

- Taxable income should be computed as per Domestic law of Source State – Nature and extent of any deductions for expenses etc. to be governed by provision of IT Act

- Withholding tax may apply as per provision of Domestic laws on gross basis.