Applicability of Article 23 – Elimination of Double taxation

In many cases, the application of tax Treaty may result into double taxation for tax payers. In such a case, in order to provide relief to such Tax payers, Article 23 provides for the mechanism through which tax credit may be available in the country of residence for taxes deducted in the souce country. Generally, credit is available only if the taxes have been rightfully deducted in the source country.

Article/Para No.

OECD Model Tax Convention on Income and on Capital 2017

UN Model Convention 2017

23A

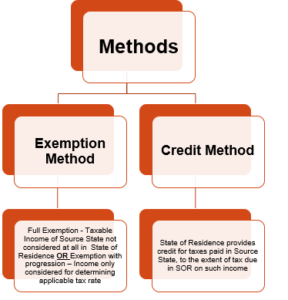

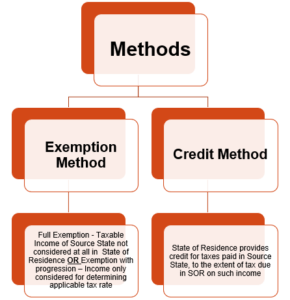

EXEMPTION METHOD

METHODS FOR THE ELIMINATION OF DOUBLE TAXATION [Article 23]

1

Where a resident of a Contracting State derives income or owns capital which may be taxed in the other Contracting State in accordance with the provisions of this Convention (except to the extent that these provisions allow taxation by that other State solely because the income is also income derived by a resident of that State or because the capital is also capital owned by a resident of that State), the first-mentioned State shall, subject to the provisions of paragraphs 2 and 3, exempt such income or capital from tax.

Where a resident of a Contracting State derives income or owns capital which may be taxed in the other Contracting State in accordance with the provisions of this Convention (except to the extent that these provisions allow taxation by that other State solely because the income is also income derived by a resident of that State or because the capital is also capital owned by a resident of that State), the first-mentioned State shall, subject to the provisions of paragraphs 2 and 3, exempt such income or capital from tax.

Under this method, also called the full exemption method , the doubly taxed income does not forms a part of income in the State of Residence. India generally does not follow full exemption method.

2

Where a resident of a Contracting State derives items of income which, in accordance with the provisions of Articles 10 and 11 (except to the extent that these provisions allow taxation by that other state solely because the income is also income derived by resident of that state), may be taxed in the other Contracting State, the first-mentioned State shall allow as a deduction from the tax on the income of that resident an amount equal to the tax paid in that other State. Such deduction shall not, however, exceed that part of the tax, as computed before the deduction is given, which is attributable to such items of income derived from that other State.

2. Where a resident of a Contracting State derives items of income which, in accordance with the provisions of articles 10, 11, 12 and 12A, may be taxed in the other Contracting State, the first-mentioned State shall allow as a deduction from the tax on the income of that resident an amount equal to the tax paid in that other State. Such deduction shall not, however, exceed that part of the tax, as computed before the deduction is given, which is attributable to such items of income derived from that other State.

UN & OECD Models:

Article 23A(2) of the OECD Model differs from Article 23A(2) in the UN Model, to the extent that OECD Model does not refer to Article 12 and 12A. This is on account of the fact that as per the OECD Model, royalties are taxable only in the State R.

3

Where in accordance with any provision of the Convention income derived or capital owned by a resident of a Contracting State is exempt from tax in that State, such State may nevertheless, in calculating the amount of tax on the remaining income or capital of such resident, take into account the exempted income or capital.

3. Where in accordance with any provision of this Convention income derived or capital owned by a resident of a Contracting State is exempt from tax in that State, such State may nevertheless, in calculating the amount of tax on the remaining income or capital of such resident, take into account the exempted income or capital.

Article 23A(3) of the OECD Model is similarly worded as Article 23A(3) deals with exemption with progression method, under which income earned in the Source Country, is exempt from tax in the Country of residence, but is included for the purpose of computing the tax rate applicable on the remaining income.

4

The provisions of paragraph 1 shall not apply to income derived or capital owned by a resident of a Contracting State where the other Contracting State applies the provisions of the Convention to exempt such income or capital from tax or applies the provisions of paragraph 2 of Article 10 or 11 to such income.

The provisions of paragraph 1 shall not apply to income derived or capital owned by a resident of a Contracting State where the other Contracting State applies the provisions of the Convention to exempt such income or capital from tax or applies the provisions of paragraph 2 of Article 10, 11, 12 or 12A to such income; in the latter case, the first mentioned State shall allow the deduction of tax provided for by paragraph 2.

The Article is identically worded in UN and OECD Model, except for difference highlighted in BOLD, Article 23A(4) intends to avoid double non-taxation of income where the Two Contracting parties differ on the facts of a case or on the interpretation of Treaty provisions . It provides that where the State of Source does not tax an income on account of certain interpretation of the convention, Resident State has the right to tax such income or capital

However, State of Residence must exempt income where Source State has the right to tax an item of income or capital but it had not imposed such tax since no tax is actually payable on such income or capital under its domestic laws.

23B

CREDIT METHOD

CREDIT METHOD

1

Where a resident of a Contracting State derives income or owns capital which, in accordance with the provisions of this Convention (except to the extent that these provision allow taxation by that other State solely because the income is also income derived by a resident of the State or solely because the capital is also capital owned by a resident of that State), may be taxed in the other Contracting State, the first-mentioned State shall allow:

a) as a deduction from the tax on the income of that resident, an amount equal to the income tax paid in that other State;

b) as a deduction from the tax on the capital of that resident, an amount equal to the capital tax paid in that other State.

Such deduction in either case shall not, however, exceed that part of the income tax or capital tax, as computed before the deduction is given, which is attributable, as the case may be, to the income or the capital which may be taxed in that other State.

Where a resident of a Contracting State derives income or owns capital which, in accordance with the provisions of this Convention (except to the extent that these provision allow taxation by that other State solely because the income is also income derived by a resident of the State or solely because the capital is also capital owned by a resident of that State), may be taxed in the other Contracting State, the first-mentioned State shall allow:

a) as a deduction from the tax on the income of that resident, an amount equal to the income tax paid in that other State;

b) as a deduction from the tax on the capital of that resident, an amount equal to the capital tax paid in that other State.

Such deduction in either case shall not, however, exceed that part of the income tax or capital tax, as computed before the deduction is given, which is attributable, as the case may be, to the income or the capital which may be taxed in that other State.

Article 23B(1) of the UN/OECD Model incorporates the principles in Article 23A(2) of the UN Model.

Under the credit method, Country of Residence retains the right to tax foreign income, but it allows credit for the taxes paid in the Source Country : –

Determine the resident’s worldwide income (including foreign sourced income) and compute tax liability .

Grant a deduction in respect of foreign tax paid on the foreign sourced income as under : –

Tax payable in Country of Residence > Taxes paid in the Source Country – Differential tax to be paid in the Country of Residence.

Tax payable in Country of Residence < Taxes paid in the Source Country – Excess tax credit may be carried forward or lapse. In India, such excess credit lapses.

2

Where in accordance with any provision of the Convention income derived or capital owned by a resident of a Contracting State is exempt from tax in that State, such State may nevertheless, in calculating the amount of tax on the remaining income or capital of such resident, take into account the exempted income or capital.

Where, in accordance with any provision of this Convention, income derived or capital owned by a resident of a Contracting State is exempt from tax in that State, such State may nevertheless, in calculating the amount of tax on the remaining income or capital of such resident, take into account the exempted income or capital.

Article 23B(2) of the OECD/UN Model Convention , permits the State of Residence to consider the exempt income in arriving at the effective tax rate on remaining income or capital of such resident.

Unilateral Relief – Section 91

What should be derived ? Income accrued outside India, which is not deemed to accrue or arise in India

Who is covered ? Person Resident in India

Which country should income arise With whom India does not have a agreement u/s 90

Manner of payment of tax Deduction or otherwise

Quantum of relief Tax deducted or Indian rate of tax, whichever is lower or IRT if both are equal

Learn More about “Article 23 – Elimination of Double Taxation” – Subscribe International Tax Course

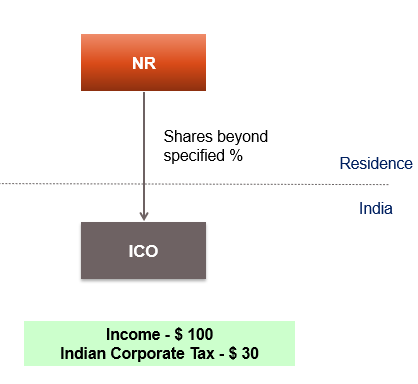

Underlying Credit

In present case, taxes may be paid by :-

ICO; and

Shareholders on dividend distributed out of remaining

For underlying credit clause, State of Residence grants credit of : –

Corporate taxes paid by ICO $ 30;

WHT on dividends $ 7.

India USA Treaty Clause : –

“in the case of a United States company owning at least 10 per cent of the voting stock of a company which is a resident of India and from which the United States company receives dividends, the income-tax paid to India by or on behalf of the distributing company with respect to the profits out of which the dividends are paid”

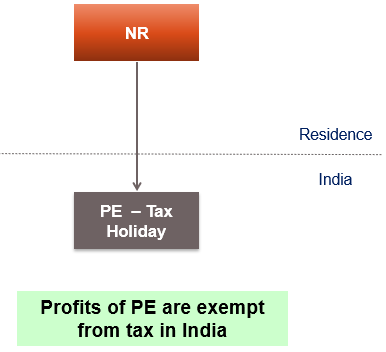

Tax Sparing

Where India grant incentives and exempt profits of NR from tax in India, if Residence State tax such profits, no benefit shall accrue to the Investors

Treaty partners may agree to forego taxes which have been spared under the incentive programmes in Source State by either : –

Exempting them from tax or

Providing deemed credit for taxes not levied by Source State

Learn More about “Article 23 – Elimination of Double Taxation” – Subscribe International Tax Course

Methods of Providing Credit – Elimination of Double Taxation – Article 23

Article 25(1) – India USA Treaty – Credit by USA

In accordance with the provisions and subject to the limitations of the law of the United States (as it may be amended from time to time without changing the general principle hereof),

the United States shall allow to a resident or citizen of the United States as a credit against the United States tax on income —

a. the income-tax paid to India by or on behalf of such citizen or resident ; and

b. in the case of a United States company owning at least 10 per cent of the voting stock of a company which is a resident of India and from which the United States company receives dividends, the income-tax paid to India by or on behalf of the distributing company with respect to the profits out of which the dividends are paid.

For the purposes of this paragraph, the taxes referred to in paragraphs 1(b) and 2 of Article 2 (Taxes Covered) shall be considered as income taxes.

Key Features

Credit shall be in accordance with/ subject to the limitations of the law of United States

Credit available to resident or citizen of the United States

Credit against the United States tax (taxes referred to in paragraphs 1(b) and 2 of Article 2 (Taxes Covered))

Credit for income-tax paid to India by or on behalf of such person – Underlying credit also available

Article 25(2) – India USA Treaty

Where a resident of India derives income which, in accordance with the provisions of this Convention, may be taxed in the United States,

India shall allow as a deductionfrom the tax on the income of that resident an amount equal to the income-tax paid in the United States, whether directly or by deduction.

Such deduction shall not, however, exceed that part of the income-tax (as computed before the deduction is given) which is attributable to the income which may be taxed in the United States.

Further, where such resident is a company by which a surtaxis payable in India, the deduction in respect of income-tax paid in the United States shall be allowed in the first instance from income-tax payable by the company in India and as to the balance, if any, from surtax payable by it in India.

Learn More about “Article 23 – Elimination of Double Taxation” – Subscribe International Tax Course

Key Features

Tax on income should be in accordance with the provisions of this Convention

Deduction for US tax limited to income-tax which is attributable to income which may be taxed in the United States

Surplus tax paid in US after set off of income tax at Bullet 2 is adjustable against surtax payable in India

Example on Credit Method – Quantum

Particulars

Amount

Total Fee for Technical Services (FTS)

200,000

Total WHT on FTS in State of Source @ 10% on gross basis

20,000

Indian tax on FTS on “Net income” basis – Situation 1

30,000

Indian tax on FTS on “Net income” basis – Situation 2

10,000

Article 25(3) – India USA Treaty – Where Does Income Arise

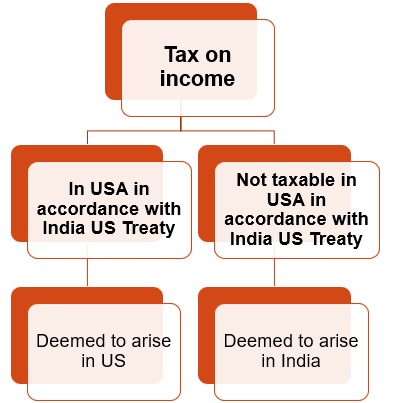

For the purposes of allowing relief from double taxation pursuant to this article, income shall be deemed to arise as follows :

a. income derived by a resident of a Contracting State which may be taxed in the other Contracting State in accordance with this Convention [other than solely by reason of citizenship in accordance with paragraph 3 of Article 1 (General Scope)] shall be deemed to arise in that other State ;

b. income derived by a resident of a Contracting State which may not be taxed in the other Contracting State in accordance with the Convention shall be deemed to arise in the first-mentioned State.

Notwithstanding the preceding sentence, the determination of the source of income for purposes of this Article shall be subject to such source rules in the domestic laws of the Contracting States as apply for the purpose of limiting the foreign tax credit.

Determination of source of income for this Article shall be subject to such “Source rules in the domestic laws of the Contracting States for the purpose of limiting the foreign tax credit”.

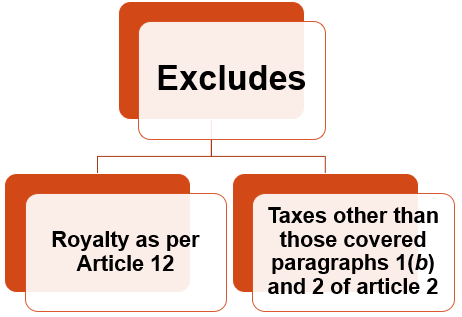

Article 25(3) – India USA Treaty – Non Applicability

The preceding sentence shall not apply with respect to income dealt with in article 12 (Royalties and Fees for Included Services).

The rules of this paragraph shall not apply in determining credits against United States tax for foreign taxes other than the taxes referred to in paragraphs 1(b) and 2 of article 2 (Taxes Covered).

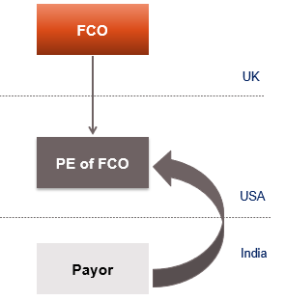

Triangular Treaty Cases

Whether tax shall be withheld as per India USA or India UK ? Should UK give a credit for such taxes ?

Learn More about “Article 23 – Elimination of Double Taxation” – Subscribe International Tax Course

Other Aspects Worth Knowing – Elimination of Double Taxation – Article 23

Is evidence for payment of tax required ? Yes, to claim credit either a TDS certificate or other original document

What if taxation is under a different head of income ? Immaterial to claim credit

Should credit be considered for Advance Tax Yes

For net of tax contract, can credit be claimed ? It is available for entire TDS

Which Year would credit be available ? When corresponding income is offered to tax in State of Residence

Can the relief be claimed on total foreign income ? Generally relief is to be claimed on income by income basis

Which taxes are creditable ? Covered by Article 2

Would State R give refund of excess tax paid in Source State No – Some countries permit carry forward of unused foreign credit

Impact of Various Events in Source State on Credit/ Exemption of Taxes

Time of payment in Source State not relevant

Losses in Source State can be deducted against foreign income, subject to domestic provision, if the income is not exempted from tax in State of Residence

If income is exempt/wrongly taxed in Source State, no credit is to be given by State of Residence for tax paid therein

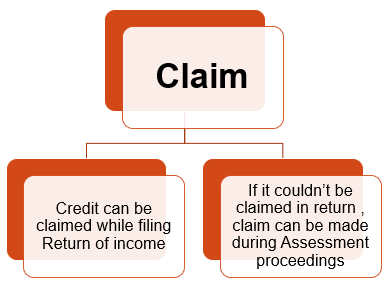

How can one claim credit?

Learn More about “Article 23 – Elimination of Double Taxation” – Subscribe International Tax Course

Have query and need a consultation with

tax expert?

We provide consultation to resolve your queries in the Area of International Tax, Merger, Demerger and Foreign Investment, though call with our Tax Expert Mr. Arinjay Jain.